The International Accounting Standards Board (IASB) has recently issued narrow scope amendments to address emerging issues in the financial landscape that took effect on 1 January 2026.

For businesses, the amendments are expected to streamline the way organisations measure and disclose financial assets and liabilities, covering modern financial instruments and complex business transactions, particularly those that are linked with ESG features and electronic payments.

For auditors and accountants, the amendments that come into effect early this year call for a more prudent approach to better evaluate their impact on the classification tests and period-end cut-off procedures.

For local guidance and applicability, the Accounting Standards Council (ASC) has released Annual Improvement to SFRS(I)s and FRSs, aligning the amendments to local contexts.

These updates focus on:

- Classification of financial assets with ESG-linked features

- Clarification of the “solely payments of principal and interest” (SPPI) criterion

- Improved disclosures for investments in equity instruments designated at fair value through other comprehensive income (FVOCI)

Key Implications

1. Clarification of the SPPI Criterion

Under FRS 109 para 4.1.2(b) and 4.1.2A(b), financial assets are measured at amortised cost or FVOCI only if they pass the SPPI test. The amendments refine the assessment of whether contractual cash flows meet the SPPI test, which is critical for determining whether a financial asset can be measured at amortised cost or FVOCI.

Key clarifications

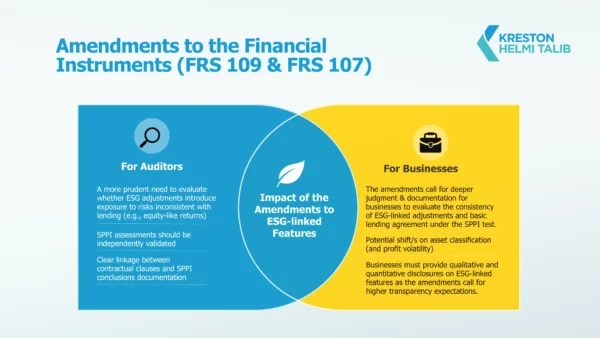

A. ESG-linked features

Previously, it was unclear if a "step-up" or "step-down" in interest rates based on achieving an ESG target made the cash flows inconsistent with a basic lending arrangement. Amendment clarifies that ESG-linked features:

-

- Do not automatically fail SPPI

- Must be assessed against a “basic lending arrangement” benchmark

ESG-linked features are consistent with SPPI if:

-

-

- The resulting cash flows are not significantly different from a comparable instrument without the feature

- The trigger is specific to the borrower (e.g., emissions targets), not external market variables.

-

B. Non-recourse features

A non-recourse instrument is one where the lender’s claim is limited to specified assets or cash flows.

The standard requires a “look-through approach”:

-

- You cannot assess SPPI based only on the legal form of the loan

- You must evaluate the underlying assets or cash flow pool

Clarification reinforces that:

-

- The economic substance of underlying assets drives classification

- Legal isolation (non-recourse) does not shield the instrument from SPPI failure

C. Contractually linked instruments (CLI)

CLIs are structured instruments with tranches, where:

-

- Cash flows are distributed in a predefined hierarchy

- Different tranches absorb risk differently

Auditor shall assess whether:

-

- The underlying pool consists of SPPI-compliant assets

- The tranche itself only exposes the holder to:

- Credit risk

- Time value of money

- Other basic lending risks

2. Electronic Settlement of Liabilities

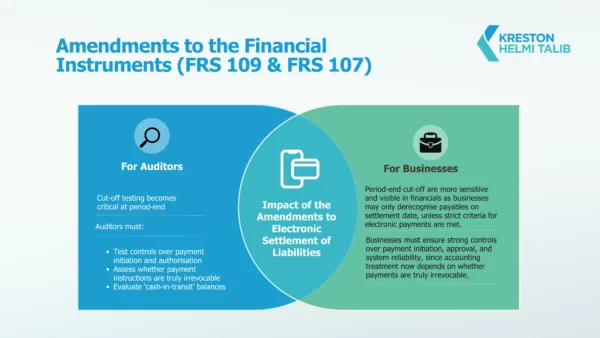

Under FRS 109 para 3.3.1, a financial liability is derecognised when it is extinguished. Extinguishment occurs when the obligation is discharged, cancelled, or expires. Amendments clarified that:

-

- Financial assets/liabilities settled via electronic systems (e.g., real-time gross settlement, digital wallets) now have explicit derecognition rules. Derecognition occurs on the settlement date (when cash is transferred).

- An entity may derecognise a financial liability before settlement date when using an electronic payment system if all of the following are met:

- Entity has no practical ability to withdraw, stop, or redirect the payment

- Payment instruction is irrevocable

- Settlement risk is insignificant

3. FRS 107 Disclosure Enhancements

The amendments to FRS 107 Financial Instruments: Disclosures do not fundamentally change the structure of disclosures, but they significantly deepen the level of transparency required, especially for:

-

- ESG-linked instruments

- Contingent and structured features

- Areas involving significant judgment (e.g., SPPI assessments)

Entities must disclose information that enables users to evaluate:

-

- The importance of financial instruments to financial position and performance

- How those instruments affect profit or loss and OCI

This includes:

-

- Carrying amounts by measurement category (amortised cost, FVOCI, FVTPL)

- Gains and losses recognised

- Reclassification impacts

The amendments highlight that for complex instruments, disclosure should go beyond numbers to explain:

-

- Why instruments are classified as they are

- What features drive their measurement outcomes

These amendments are narrow in scope but broad in impact.

For accountants, the challenge lies in classification accuracy, derecognition timing, and disclosure completeness.

From an audit perspective, the changes increase the need for:

- Careful evaluation of contractual cash flow characteristics

- Strong documentation of judgments

- Enhanced scrutiny of disclosures