The Institute of Internal Auditors (IIA) unveiled its updated Global Internal Audit Standards on 9 January 2024, offering a modernised and comprehensive framework designed to enhance internal audit functions and foster positive organisational change. Adopting these new standards allows organisations to adapt to the fast-paced evolution of business environments, technological innovations, and emerging risks.

Effective 9 January 2025, this new standard will replace the 2017 International Standards for the Professional Practice of Internal Auditing (ISPPIA). The 2017 standards remain in effect during the 12-month transition period.

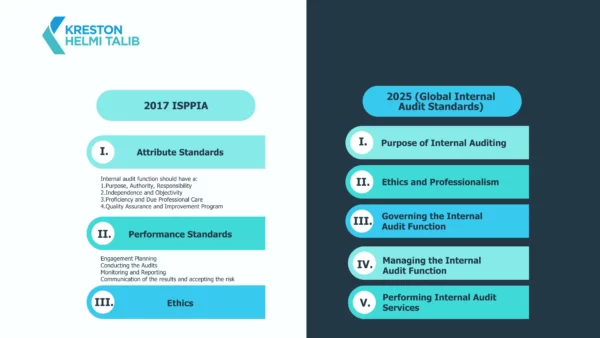

Whilst the 2017 International Standards for the Professional Practice of Internal Auditing (ISPPIA) highlights the purpose, authority, and responsibilities of internal auditors along with detailed notes on performance standards and ethics, the new standard provides a more comprehensive and holistic approach to internal audit functions. In a nutshell, the comparison between the two standards can be found below:

The new standards have provided a detailed view of the internal audit functions.

Domain I: Purpose of Internal Auditing

- Internal auditing enhances the organization’s successful achievement of its objectives, governance, risk management and control processes, decision-making and oversight, reputation and credibility with its shareholders, and ability to serve the public interest.

- Internal auditing is most effective when it is performed by competent professionals in conformance with the Global Internal Audit Standards. The internal audit function is independently positioned with direct accountability to the board.

Domain II: Ethical and Professionalism

- Fundamental Principles

- Integrity

- Objectivity

- Professional Competence

- Confidentiality

- Professional Behavior

- Conflict of Interest

- Communication objectively and reporting unethical or illegal activities

Domain III: Governing the Internal Audit Function

- The board establishes, approves, and supports the mandate of the internal audit function.

- The board establishes and protects the internal audit function’s independence and qualifications.

- The board oversees the internal audit function to ensure the function’s effectiveness.

Domain IV: Managing the Internal Audit Function

- The chief audit executive plans strategically to position the internal audit function to fulfill its mandate and achieve long-term success.

- The chief audit executive manages resources to implement the internal audit function’s strategy and achieve its plan and mandate

- The chief audit executive guides the internal audit function to communicate effectively with its stakeholders.

- The chief audit executive is responsible for the internal audit function’s conformance with the Global Internal Audit Standards and continuous performance improvement.

Domain V: Performing Internal Audit Services

- Internal auditors plan each engagement using a systematic, disciplined approach.

- Internal auditors implement the engagement work program to achieve the engagement objectives.

- Internal auditors communicate the engagement results to the appropriate parties and monitor management’s progress toward the implementation of recommendations or action plans.

Key Takeaways:

- Enhanced framework: The new standards offer a more comprehensive and streamlined framework for internal audit.

- Focus on value creation: The standards emphasize the role of internal audit in creating, protecting, and sustaining value for organizations.

- Ethical principles: The standards reinforce the importance of ethical conduct and professionalism in internal auditing.

- Governance and oversight: The standards provide guidance on the governance and oversight of internal audit functions.

- Continuous improvement: The standards emphasize the need for continuous improvement and adaptation to changing business environments.

By adopting and implementing the Global Internal Audit Standards, organizations can strengthen their internal audit functions, improve risk management, and enhance their overall governance and performance.

________________________________________________________________________________________________________________________________

All materials have been prepared for general information purposes only. The information presented in this document is not legal advice, is not to be acted on as such, may not be current and is subject to change without notice. Professional advisory should be sought before taking or refraining from any action as a result of the contents of this document. Details are based on the information as of 01 December 2024.