Singapore Standards in Auditing (SSA) 600 Special Consideration – Audits of Group Financial Statement

Effective 15, December 2023, the revised Singapore Standards in Auditing (SSA) 600 Special Considerations on Audit of Group Financial Statements will be the governing guidelines for an audit of group financial statements, including the circumstances when component auditors are involved.

The revision aims to:

(1) Enhance the group auditors’ accountability for exercising professional skepticism,

(2) Strengthen the group auditors’ approach to planning and executing group audits,

(3) Improve communication between the group auditor and component auditors in a two-way communication manner; and

(4) Boost the documentation practices involved in the auditing process. Access the full revised standards in this link.

The Role of the SSA 600 Revisions to a Better Quality Management

The changes made to the Revised SSA 600 sought to achieve the following:

1. Nurturing a Preventive Approach to Quality Management

Risk-based Approach

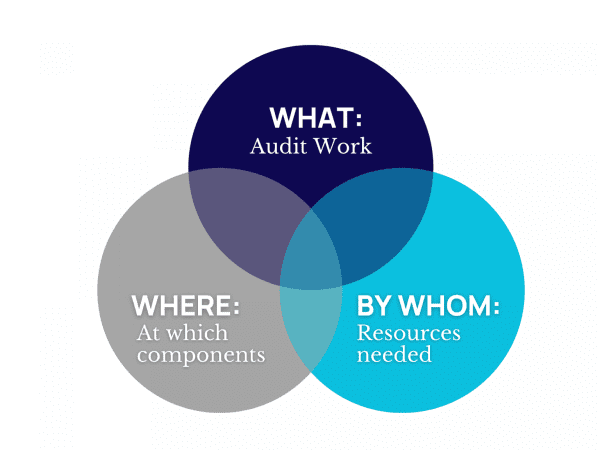

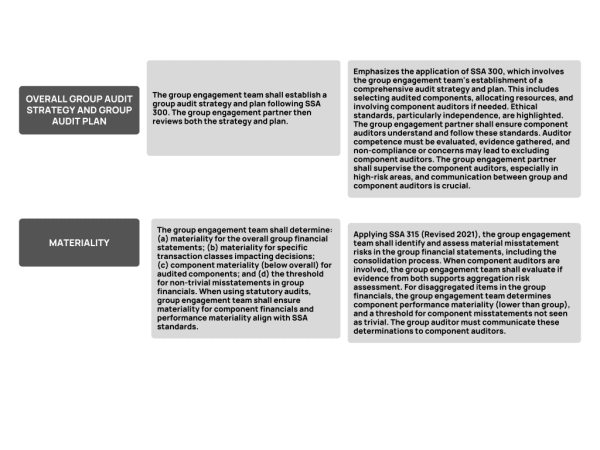

In extant SSA 600, the group auditor identifies “significant component/(s)” of the group and performs an audit of the financial information of these components. In the revised standard, the concept of “significant component” is removed. Instead, the revised standard introduces a new approach for planning and performing a group audit engagement, referred to as the risk-based approach.

The introduction of this approach provides:

- Greater alignment with the requirements of SSA 315 (Revised) and SSA 330.

- Greater focus on identifying and assessing the risks of material misstatements.

- Greater focus on designing and performing the corresponding and appropriate audit procedures to address those identified risks.

This new approach helps the group auditor to re-evaluate its group audit strategy, enhancing the audit quality and effectiveness of group audits.

Managing and Achieving Quality in Group Audits

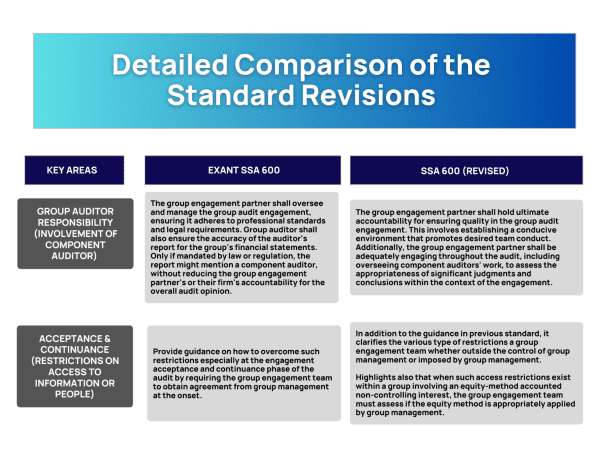

The standard also provides clarification on requirements on SSQM 1 – Quality Management for Firms that Perform Audits or Reviews of Financial Statements, or Other Assurance or Related Services Engagements, and SSA 220 (Revised) – Quality Management for an Audit of Financial Statements. The standard elucidates the sufficient and appropriate resources in a group audit, including the involvement of component auditors and matters that require consideration in determining the direction and supervision of the engagement team and review of their work.

Restrictions on Access to Information and People

The revised standard laid out the various types of restrictions that could potentially impact the audit process, such as access to people and information, component auditor’s audit documentation and legal or regulatory restrictions, as well as, guidance notes on how to overcome those restrictions, such as to provide more robust assurance on the group audit. SSA 600 also emphasizes the importance of open communication and early identification of restrictions to mitigate the impact on the audit process.

Materiality

The revised standard emphasizes that aggregation risk is particularly important to understand and address in a group audit because there is a greater likelihood that audit procedures will be performed on classes of transactions, account balances or disclosures that are disaggregated across components. The higher the number of components at which audit procedures are performed, the greater the aggregation risks.

In setting up the component materiality, the extent of disaggregation of the financial information across components should be considered to reduce the aggregation risk to an appropriate low level.

2. Elevating Professional Skepticism

In the context of the standard, professional skepticism is a key element that strengthens the group audit process. The engagement team of the group audit, including component auditors, is expected to plan and perform the audit with professional skepticism and exercise professional judgment. The group auditor shall remain alert for any inconsistent information from component auditors, component management, and group management that may be significant to the group financial statements, and be conscious of potential biases that may hinder the exercise of professional skepticism.

3. Empowering Audit Documentation for Enhanced Consistency

Underscoring the significance of the group auditor’s review of the component auditor audit documentation, the standard aims to strengthen the quality and consistency of the group audit. Well-documented audit trail helps facilitate the effective review process, both internally within the audit firm and externally by regulatory bodies or peer reviewers.

The review of component auditor work ensures that the group auditor has a complete understanding of the audit procedures performed at the component level and can form a reliable opinion on the group’s consolidated financial statements.

The review of component auditor work ensures that the group auditor has a complete understanding of the audit procedures performed at the component level and can form a reliable opinion on the consolidated financial statements of the group.

4. Fostering Dynamic Collaboration

The standard heightened emphasis on establishing strong two-way communication between the group auditor and the component auditor(s) involved in a group audit. A proactive risk-based approach helps address the potential challenges or differences early on, reducing the risk of misunderstandings and ensuring that the group audit engagement runs smoothly and effectively. It encourages both group and component auditors to actively collaborate, exchange information, and share perceptions to ensure a comprehensive and well-coordinated audit process.

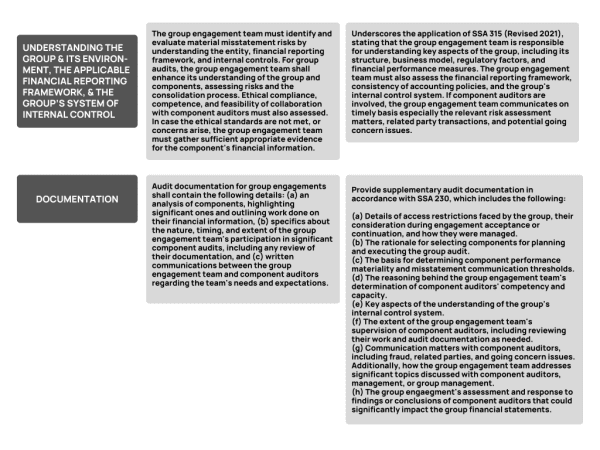

For a snapshot view of the changes in the existing standard, summarised below are the key areas of changes and the descriptive revisions of each.

Keeping abreast with the new and upcoming standards keeps us equipped with the necessary technical knowledge, skills, and expertise to perform quality service.

For more information about the revision, reach out to Roda or Airey from the Business Development Team.

All materials have been prepared for general information purposes only. The information presented in this document is not legal advice, is not to be acted on as such, may not be current, and is subject to change without notice. Professional advisory should be sought before taking or refraining from any action as a result of the contents of this document.