The proposed ISSA 5000 is designed to be a comprehensive and independent standard applicable to limited and reasonable sustainability assurance engagements. The proposal is more specific than ISAE 3000 (Revised) and ISAE 3410 for sustainability priority areas. It will cover sustainability information reported on various topics and prepared under multiple frameworks, including the IFRS Sustainability Disclosure Standards S1 and S2.

The anticipated approval of the standard is expected to be before the end of 2024.

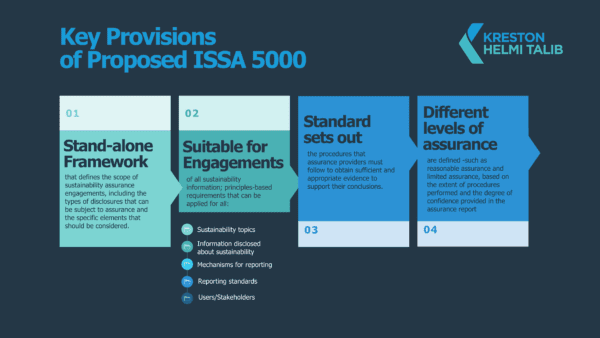

Key Provisions of Proposed ISSA 5000

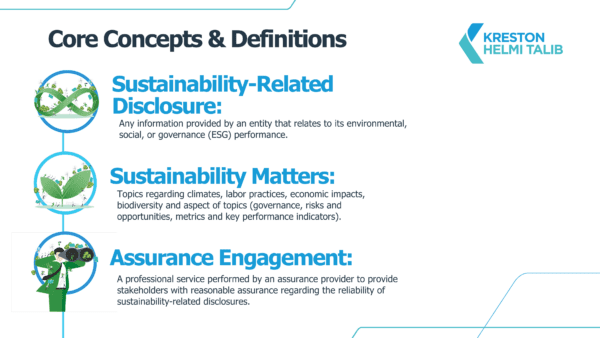

Core Concepts and Definitions

ISSA 5000 introduces several key concepts and definitions:

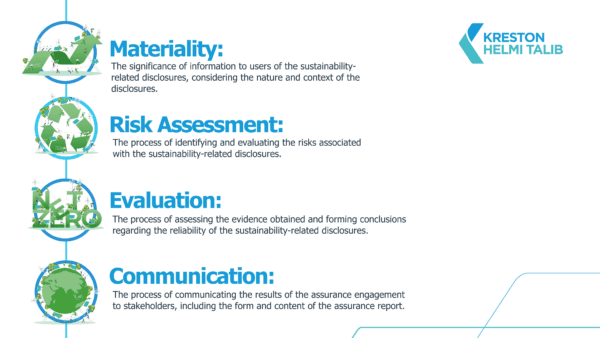

Risk assessment, evaluation, and communication are essential for the credibility of sustainability disclosures. By identifying risks, evaluating evidence, and communicating results, organisations build stakeholder trust and show their commitment to sustainability. As the importance of sustainability continues to grow, so too does the need for robust assurance engagements that uphold the highest standards of accountability and transparency.

All materials have been prepared for general information purposes only. The information presented in this document is not legal advice, is not to be acted on as such, may not be current and is subject to change without notice. Professional advisory should be sought before taking or refraining from any action as a result of the contents of this document. Details are based on the information as of 01 September 2024.